Through the Lens of the CEO: Why SoFi's Banking License is it's Secret Weapon

A First Look at the Business: SoFi Technologies Inc.

Hi, everyone, I'm Felix, and today I’m stepping into Anthony Noto's shoes. Last month's earnings call proved something that most investors still don't understand: SoFi isn't just another fintech, we're building the financial infrastructure for America's next generation. Here's why our competitors are playing checkers while we're playing chess.

Overview

Today, I’ll discuss the following things through the eyes of Anthony Noto:

Products

Market Position

Revenue Model

Competitive Position

Growth Strategy

Introduction: The strategic tension wall street doesn't see

I'm Felix, and today I'm thinking like Anthony Noto, CEO of SoFi Technologies. Three weeks ago, when we announced our Q4 2024 results (revenue growth of 17% with a gross profit margin of 82.1%), I watched the market's reaction with fascination. The stock jumped, analysts celebrated, but I realised most people still don't understand what we've actually built here.

Here's the controversial truth that keeps me up at night: every traditional bank and fintech competitor is fighting yesterday's war. They're obsessing over customer acquisition costs and loan origination volumes while we've quietly constructed something they can't replicate (a full-stack financial operating system with our own banking license).

The strategic dilemma is real: Do we accelerate growth by playing their game, or do we continue building our moat even if it means slower near-term expansion?

Most CEOs would chase the quick growth. I've chosen the harder path, and it's about to pay off in ways Wall Street hasn't priced in.

"2024 was undoubtedly SoFi's best year ever," I told investors in January, but that's not the whole story. The real story is that while Upstart burns cash trying to perfect AI lending and Marcus by Goldman Sachs retreats from consumer banking, we're building sustainable competitive advantages that compound over time.

This isn't about beating earnings estimates, it's about creating a financial ecosystem that becomes more valuable as it grows. Here's why this challenge actually proves our competitive strength: regulatory complexity and execution requirements create barriers that prevent competitors from replicating our model. Understanding our strategic positioning sets up the critical question: Is now the right time to invest? I'll answer that in this week's technical analysis.

Our Products: strategy & market reality

Most financial services companies are trapped in single-product thinking. Upstart lives and dies by their AI lending algorithms. Rocket Companies dominates mortgages but struggles elsewhere. Marcus by Goldman Sachs tried to be everything to everyone and ended up retreating from key markets.

| Seeking Alpha")

While competitors focus on optimising single products, we're capturing 1.4 products per customer on average because we built a financial flywheel where each service strengthens the others. When someone starts with a SoFi personal loan, they discover our 3.80% APY savings account. That high-yield savings relationship leads to our credit card, investment platform (which offers zero commission trading like Robinhood but with comprehensive financial planning tools that Interactive Brokers charges premium fees for), and eventually our mortgage and insurance products.

Most investors miss this, but our product roadmap positions us for the massive intergenerational wealth transfer happening over the next decade while competitors are still fighting over loan origination volumes in commoditized markets. Our multi-product members have 3x higher lifetime value than single-product users, and they churn at half the rate.

Here's what changes everything: our banking license is the secret weapon that makes this flywheel possible. When you can hold deposits, you control the funding cost equation.

Traditional lenders like LendingClub and Prosper are at the mercy of capital markets for funding. When credit tightens, their margins compress. We fund our lending through our own deposit base, giving us both cost advantages and strategic flexibility.

Risk acknowledgment is critical here. The multi-product strategy requires massive upfront investment and perfect execution across multiple financial verticals. One product failure could damage trust across the entire ecosystem. But that's exactly why competitors can't replicate what we've built (the execution complexity is our competitive moat).

Our Market Position: opportunity & competitive chess match

The $4.5 trillion consumer banking market sounds big, but here's what others miss about the emerging segment: it's fragmenting faster than anyone realizes, creating a window for comprehensive financial platforms to capture disproportionate market share.

Traditional banks are stuck with legacy infrastructure that makes true innovation nearly impossible. Meanwhile, single-product fintechs are discovering that customer acquisition costs have skyrocketed to unsustainable levels. We're positioned perfectly in the middle (nimble enough to innovate like a fintech, stable enough to hold deposits like a bank).

We're moving into wealth management aggressively now because rising interest rates create a 5-year window where traditional wealth managers are vulnerable to disruption. While they're charging 1%+ management fees for basic portfolio management, we're building automated investing tools that deliver better outcomes at lower costs. Unlike Robinhood's basic trading platform or Interactive Brokers' complex professional tools, we're creating investment solutions that integrate seamlessly with our banking and lending relationships.

The competitive positioning breakdown reveals the strategic opportunity. JPmorgan Chase dominates through scale but moves slowly on innovation. Bank of America has distribution but terrible digital experience. And Wells Fargo is still recovering from regulatory issues.

On the fintech side, Upstart is profitable but limited to personal loans. LendingClub pivoted to banking but lacks our product breadth.

Customer acquisition intelligence shows our advantage: while competitors spend $400-800 to acquire a customer who might use one product, we're spending similar amounts to acquire customers who use 2.8 products on average. Our customer lifetime value math is fundamentally different (and fundamentally better).

Here's the competitive reality most analysts miss: the winners in financial services will be companies that own the complete customer relationship. Apple is trying to build this with Apple Card and Apple Pay. Amazon has Amazon Pay but lacks banking capabilities. We're the only pure-play financial services company that's built the full stack with regulatory approval.

Our Revenue Model: The Engine & Financial Reality

Traditional financial services companies have linear revenue models (more loans equal more revenue, but also more risk and higher funding costs). We've built something different: a compounding revenue model where growth in one area accelerates growth everywhere else.

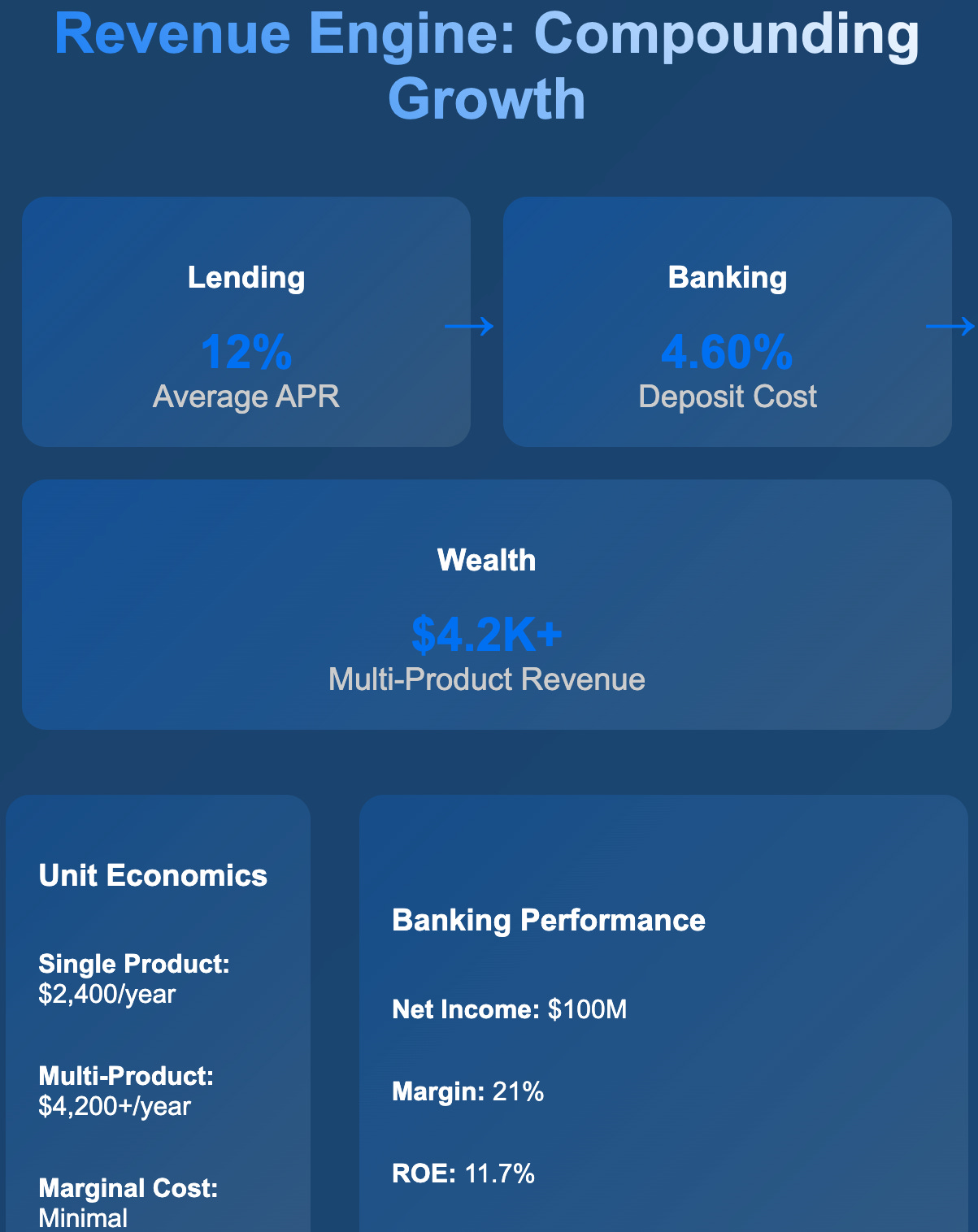

The revenue architecture tells the strategic story. Our lending segment generates the customer relationships and provides the initial revenue stream at 12% average apr. Our financial services segment (deposits, credit cards, banking products) creates the funding base at 4.60% cost and deepens customer relationships. Our technology platform segment monetizes our infrastructure by serving other financial institutions.

We're sacrificing short-term lending growth to build deposit gathering and wealth management capabilities because loans without deposits are just expensive customer acquisition, while deposits without lending opportunities are just expensive funding. The combination creates sustainable competitive advantages that compound over time.

Here's the unit economics reality that changes everything: a customer who starts with a $20,000 personal loan generates about $2,400 in annual revenue. But if they also use our high-yield savings account, credit card, and investment platform (where unlike Robinhood users who just trade, or Interactive Brokers clients who pay for advanced features, our members get comprehensive financial planning as part of their existing relationship), their annual revenue contribution jumps to $4,200+. The marginal cost to serve them across multiple products is minimal because we built shared infrastructure.

Our financial positioning gives us options competitors don't have. Our bank reported net income of $100 million with a 21% margin and a return on tangible equity of 11.7% (in Q4 2024). That banking profitability funds our technology investments and allows us to take longer-term strategic bets while competitors optimize for quarterly results.

Margin pressures are real (competition for deposits has intensified, and loan loss rates are normalizing from historically low levels). But our diversified revenue model means we're not dependent on any single margin driver. When lending margins compress, we push wealth management. When deposit costs rise, we focus on fee-based revenue.

Our Competitive Position: Moat & Strategic Vulnerability

Let me be brutally honest about our competitive position: SoFi's banking license is both our greatest strength and our highest risk. It gives us capabilities that most fintech competitors can't replicate, but it also subjects us to regulatory oversight that can constrain our growth speed.

The quantified advantages are substantial and measurable. Our cost of funds (what we pay for deposits) is dramatically lower than what asset-light lenders pay for warehouse financing. While Upstart might pay 8-10% for capital during tight credit markets, we're paying 3.80% apy to depositors who are also our customers. That 350+ basis point advantage flows directly to our bottom line.

Here's what keeps me up at night: regulatory risk is our biggest existential threat. Banking regulations change, capital requirements can increase, and examination cycles can slow our innovation. One significant regulatory issue could damage our brand across all product lines. Unlike single-product fintechs that can pivot quickly, our banking license makes us less agile in some ways.

But that regulatory burden is also our defensive moat that competitors can't easily replicate. Obtaining a banking license takes years and requires substantial capital commitment. None of our direct fintech competitors have been willing or able to go through that process. Even well-funded companies like Chime and Robinhood have chosen banking partnerships over direct banking licenses.

Our defensive strategies center on execution speed and customer experience excellence. We need to build our moat faster than competitors can build theirs. Every month we delay launching new products or improving existing ones gives competitors time to catch up or find alternative strategies.

Direct comparison with key competitors reveals our unique positioning. Upstart: higher technology sophistication but limited product scope and higher funding costs. LendingClub: similar banking capabilities but weaker brand recognition and limited product innovation. Marcus: stronger parent company but retreating from consumer markets after strategic failures.

Our Growth Strategy: Vision & Investment Thesis Setup

The strategic foundation is solid, but successful investing requires understanding our growth trajectory and resource allocation priorities. We're not just growing a lending business, we're building the financial infrastructure for America's next generation of high-earning professionals.

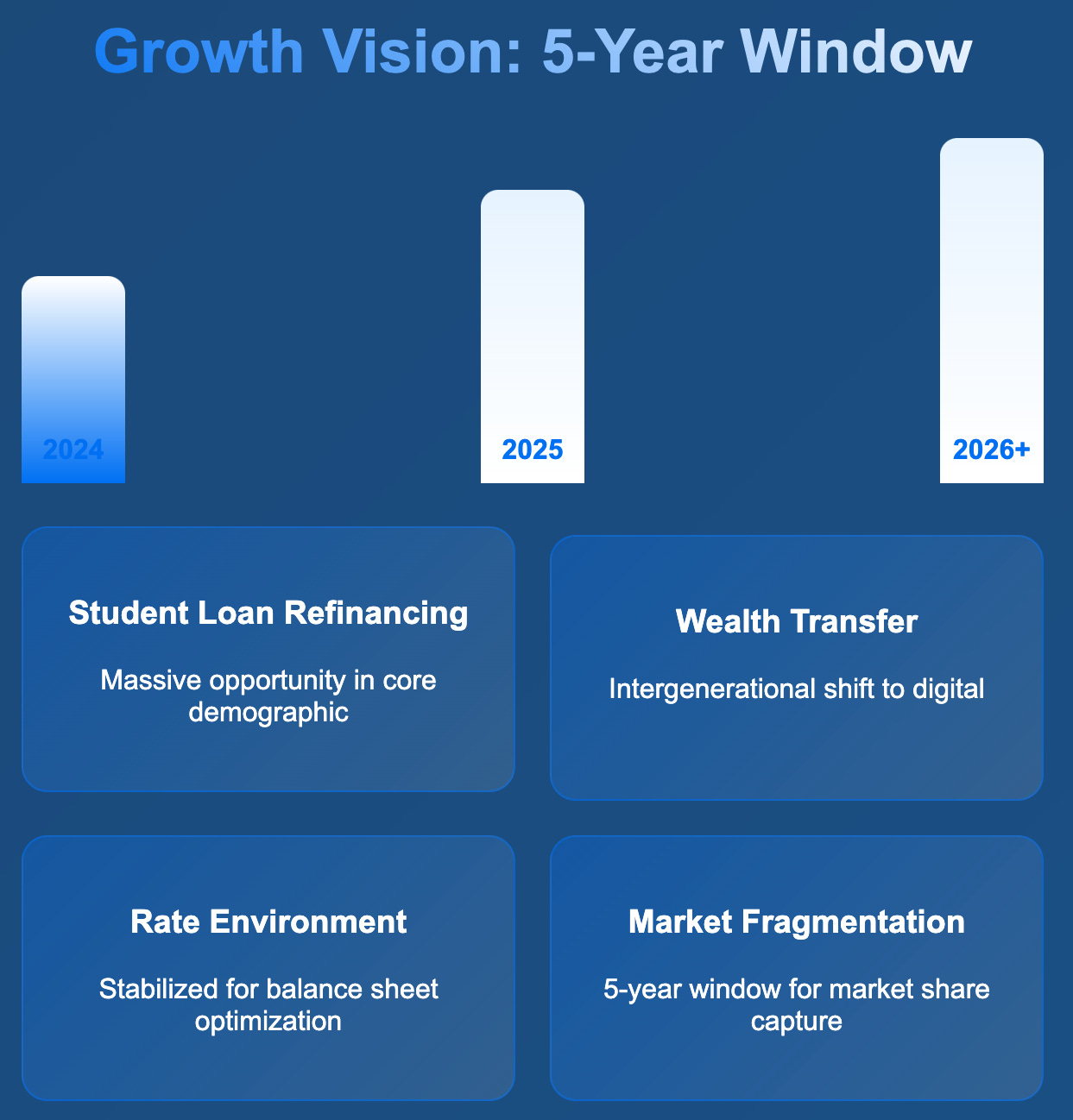

Strategic catalysts are aligning perfectly for accelerated growth. Student loan payments resumed in 2023, creating massive refinancing opportunities in our core demographic. The federal reserve's interest rate environment has stabilized, allowing us to optimize our balance sheet for profitability. Most importantly, younger consumers are increasingly willing to switch from traditional banks to digital-first financial services.

Our growth trajectory targets are ambitious but achievable based on current market trends: projected revenue growth of 17% for fy2025 and 20-25% annual eps growth beyond 2026. These aren't just financial projections, they represent our strategic roadmap for capturing market share in multiple financial verticals simultaneously.

Resource allocation priorities reveal our strategic thinking and competitive focus. We're investing heavily in technology infrastructure that serves both our direct customers and our b2b technology platform clients. We're expanding our wealth management capabilities to capture the massive intergenerational wealth transfer happening over the next decade. We're building our credit card and payment capabilities to compete directly with established players.

Risk mitigation strategies acknowledge the competitive and economic challenges ahead. We're diversifying our revenue streams to reduce dependence on interest rate cycles and economic conditions. We're building strategic partnerships with traditional financial institutions who need our technology capabilities. We're maintaining strong capital ratios to weather economic uncertainty and regulatory changes.

Market timing creates a 5-year window where the competitive landscape is still forming and market share is available for capture. Traditional banks are struggling with digital transformation costs and legacy infrastructure. Single-product fintechs are hitting growth walls as customer acquisition costs rise. Big tech companies are focused on other strategic priorities and face their own regulatory challenges.

The $10 billion revenue opportunity isn't hyperbole, it's mathematical reality. If we capture 2% of the consumer banking market with our current product mix and margin profile, we're looking at $90 billion in assets under management. With our current margin profile, that translates to $8-12 billion in annual revenue within our addressable timeframe.

This strategic foundation is solid, but successful investing requires perfect timing. The difference between buying SoFi at current levels versus waiting for a pullback could determine your entire return profile. In this week's "fundamentals meet technicals" analysis, I'll break down whether SoFi's current valuation reflects this growth potential and identify the optimal entry points for maximum returns. The technical patterns are setting up for a major directional move, and you'll want to see exactly which way the charts are pointing before making your investment decision.

If you enjoyed reading this article, and would like to read more articles like this one, you should go and check out the following:

In the coming days, I'll be publishing a comprehensive 'Fundamentals meet Technicals' analysis that dives deep into the company's financial statements while applying technical indicators to determine whether the stock presents a compelling buying opportunity. This dual-lens approach will provide you with both the fundamental backdrop and technical setup needed to make an informed investment decision.

Stay subscribed to ensure you don't miss this in-depth analysis and other valuable investment insights.

Disclaimer: here

Excellent deep dive. Thanks

Great deep dive on Sofi (a stock I like a great deal)