Kinsale Capital: The Quiet Giant That Keeps Beating Wall Street

A Deep Dive into Kinsale Capital and Why this is a (potential) Buy.

Kinsale Capital Group, a leading player in the specialty insurance sector, particularly in the Excess & Surplus (E&S) market. This segment focuses on underwriting higher risk businesses that are often not covered by standard insurers, offering tailored policies for non standard or complex risks. The company generates revenue from a variety of channels within this specialized insurance space.

Overview

Today, I’ll talk about the following:

How does Kinsale Capital make money?

Combined ratio

Excess & Surplus market

Revenue sources breakdown

Geographical revenue distribution

Future outlook

Final thoughts

If you like to discover more businesses like the one I’m discussing here, make sure to SUBSCRIBE if you want more like this!

How does Kinsale Capital make money

Kinsale generates its income primarily through the underwriting of specialty insurance policies. They write policies in the Excess and Surplus (E&S) market, which includes businesses that face non-standard risks. These can range from unusual commercial properties to complex casualty risks that traditional insurers may not want to take on.

But let’s start of by dissecting, Kinsale’s key Revenue Sources:

Net earned premiums (73% of their total revenue)

Underwriting income (17% of their total revenue)

Net investment income (8% of their total revenue)

Fee income (2% of their total revenue)

In the next section, I’ll dive deeper in each revenue source.

Net earned premiums

The majority of their revenue comes from net earned premiums. These are premiums that the company collects from its policyholders over the life of the policy.

Revenue

2024: $1.35 billion

2023: $1.07 billion

The rise in premiums reflects their strong market position and growing customer base, particularly in niche markets where their expertise in underwriting plays a critical role.

Underwriting income

Kinsale is known for its strong underwriting performance, which is reflected in its underwriting income.

Revenue

2024: $326 million

2023: $270 million

In the next section about the combined ratio, I’ll discuss their underwriting income further.

Net investment income

Like most insurance companies, they invest the premiums it receives in various securities, and earns a return on those investments.

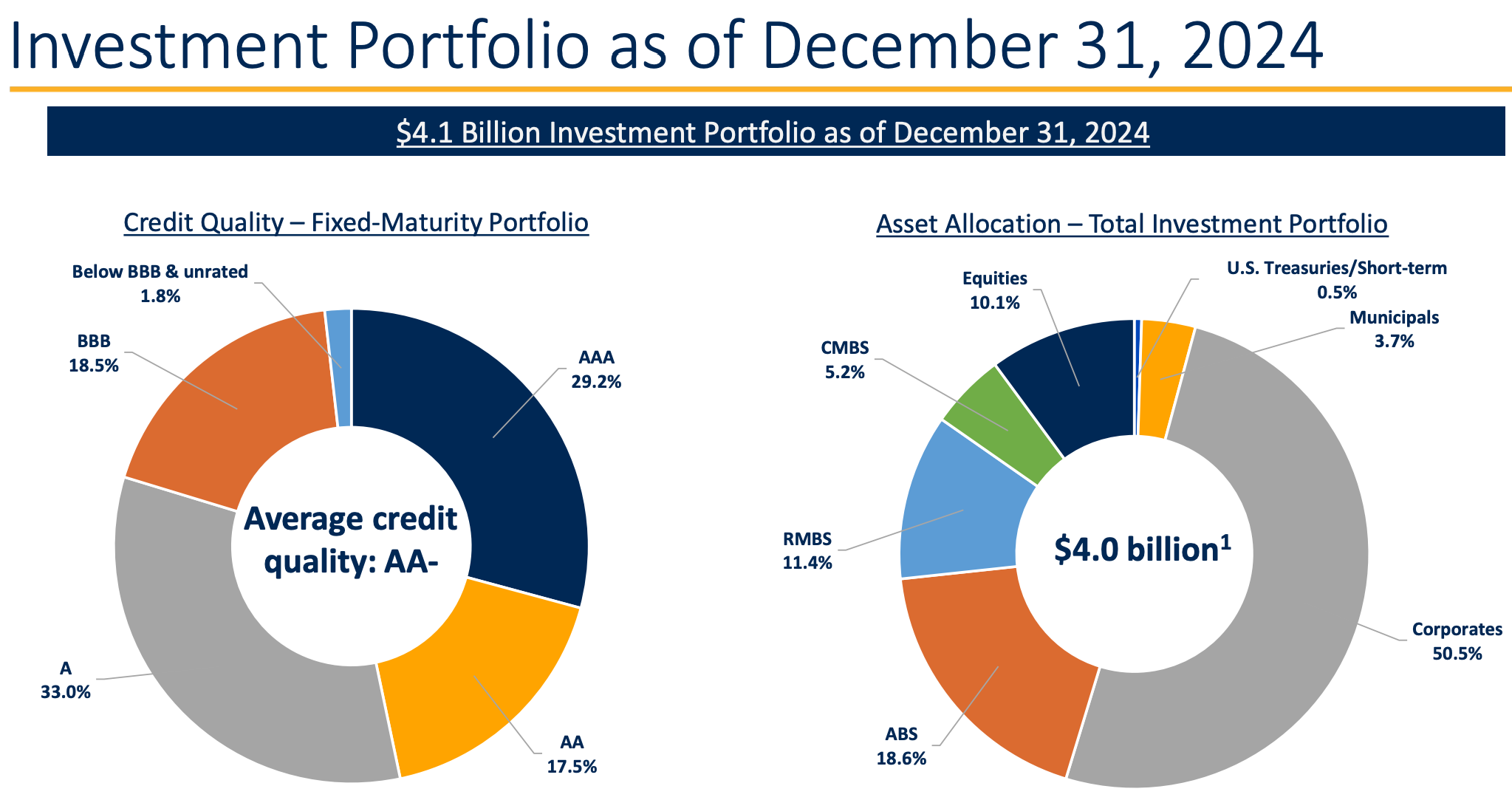

Asset Allocation:

Kinsale Capital has built up a sizable investment portfolio worth around $4 billion, which is quite significant given that it's nearly 50% of the company’s market cap and approximately four times its total shareholders’ equity. This highlights how crucial investment income is as a secondary revenue stream for insurers like Kinsale, alongside underwriting profits.

Here’s how that $4 billion is allocated:

Corporate Bonds – 50.5%

This is the largest slice of their portfolio, primarily composed of investment-grade corporate debt. These provide relatively stable returns and are typically considered lower risk compared to equities.Asset-Backed Securities (ABS) – 18.6%

These are bonds backed by pools of assets like auto loans, credit card receivables, or student loans. While they offer diversification and yield, they can carry more complexity and credit risk.Residential Mortgage-Backed Securities (RMBS) – 11.4%

RMBS are securities backed by home mortgages. While generally safe when issued by government sponsored entities, these instruments still carry interest rate risk and exposure to housing market cycles.Commercial Mortgage-Backed Securities (CMBS) – 5.2%

These are similar to RMBS but tied to income-generating commercial properties. They're often used to boost yield, though they carry greater exposure to economic conditions in real estate sectors.Equities – 10.1%

This allocation provides growth potential but comes with higher volatility. It reflects a willingness to accept more risk for long-term returns.The rest - 4.2%

U.S. Treasuries/Short-Term and Municipals

This diversified allocation strategy gives Kinsale flexibility. It helps them maintain liquidity to pay claims while also generating investment returns, a critical component of long-term insurance profitability. However, it also means they are exposed to interest rate risk, credit risk, and market volatility, especially in the fixed-income side of the portfolio.

Revenue

2024: $150 million

2023: $102 million

This income is essential for maintaining profitability, as the company can use these returns to offset underwriting costs.

Fee income

Kinsale also generates revenue from fees associated with underwriting, policy issuance, and other services.

Revenue

2024: $34 million

2023: $27 million

While this constitutes a smaller portion of their overall revenue, it contributes to the stability and diversification of their income streams.

Combined Ratio

The formula is:

Combined ratio = Loss ratio + Expense ratio

Loss ratio = claims paid out ÷ premiums earned

Expense ratio = operating expenses ÷ premiums earned

The combined ratio is one of the most important financial metrics for an insurance company like Kinsale Capital. It measures the profitability of the company's insurance operations (the "underwriting" side of the business) before factoring in investment income.

Explanation

A combined ratio under 100% means the insurer is making an underwriting profit, they’re collecting more in premiums than they’re paying out in claims and expenses.

A combined ratio over 100% means the insurer is losing money on underwriting and relies on investment income to stay profitable.

Kinsale’s combined ratio

In 2024, Kinsale reported a combined ratio of 76.4%, which is exceptionally strong. (this image got numbers from back in 2023)

For context:

Most good insurers aim for a combined ratio around 90 to 95%.

A 76% combined ratio indicates extremely profitable underwriting.

This means for every $1.00 they collect in premium, it only paid out 76.4 cents in claims and expenses combined, keeping 23.6 cents purely from underwriting, before even touching investment income.

Breakdown example

Loss ratio: 55.8% (Kinsale is excellent at underwriting profitable policies)

Expense ratio: 20.6% (relatively efficient operations for an E&S insurer)

Add them up → 55.8% + 20.6% = 76.4% (Combined Ratio)

Why it matters for Kinsale

Their ability to maintain a low combined ratio over time proves that they are very good at picking the right risks.

In the Excess & Surplus (E&S) market (where risks are non-standard and often complex), good underwriting is even more crucial.

It gives Kinsale a huge competitive advantage over peers who may either price risks too aggressively or manage expenses poorly.

Bottom line

Kinsale doesn’t just rely on investment returns like many insurers, they are profitably underwriting insurance in the first place, which is much rarer and more valuable in the long term.

This is well below 100%, indicating that Kinsale is effectively managing its insurance operations by paying out fewer claims than it collects in premiums, which is a sign of strong underwriting discipline and profitability.

You can also see that their combined ratio has been going down, which indicates that they are their management is capable of increasing their profitability at a steady pace.

Excess & Surplus market

The Excess & Surplus (E&S) insurance market plays a crucial but often overlooked role in the broader insurance world.

While traditional insurance companies (called "admitted carriers") focus on more standardized, lower risk policies — like basic home insurance or car insurance — the E&S market steps in when things get too messy, risky, or unusual.

What exactly is E&S insurance?

Imagine you want to buy insurance, like for your house or your business.

Normally, you go to a regular insurance company, simple.

But what if your situation is weird, risky, or brand new?

Maybe you live in a wildfire zone.

Maybe you run a drone delivery company.

Maybe you organize massive EDM festivals.

Regular insurers would probably say “No thanks.”

That’s when the E&S insurers step in.

They basically say:

"We’ll take the risk. But we’re going to charge you more and write our own rules."

E&S carriers are the "special forces" of insurance, covering the stuff that traditional companies avoid.

Key characteristics of the E&S market

Flexibility:

E&S insurers can quickly design policies for unusual risks because they aren’t as tightly regulated as admitted insurers.Higher premiums:

They take on tougher risks, so they charge more money to cover potential big losses. (their loss rate is around 20%)Customized coverage:

Every policy is more tailored to the individual client or situation.Fast growth:

As the world becomes more complex (cyber threats, climate change, niche industries), the E&S market keeps expanding.

In fact, in the U.S., E&S premium volume has been growing faster than the standard insurance market over the past decade (source: AM Best, 2023).

Why is the E&S Market so important?

Without it, tons of businesses and people would simply go uninsured.

It acts as a relief valve for the insurance industry, giving coverage options for hard-to-place risks.

Companies like Kinsale specialize in finding these difficult, often high margin opportunities. (net income margin: 25%)

And importantly:

E&S carriers typically enjoy better profitability because they can price risks appropriately without getting bogged down by regulations that bind traditional insurers.

Revenue Sources Breakdown

Kinsale generates its revenue across multiple business lines, each serving different industries and risk profiles.

In 2024, Kinsale’s gross written premiums amounted to $1.9 billion, with the following breakdown across its main segments:

Commercial Property

This line represents 24.4% of the company’s gross written premiums.

It includes insurance policies for various commercial property types, such as office buildings, industrial facilities, and retail establishments.

Commercial property insurance covers risks like fire, vandalism, and natural disasters, which can be difficult to insure through standard channels.

Excess Casualty

Excess casualty insurance accounts for 13.1% of gross written premiums.

This line provides coverage above the standard liability limits, protecting businesses against large, unforeseen claims that exceed traditional policy limits.

It’s particularly relevant for high risk industries where accidents and lawsuits are more likely, such as construction or manufacturing.

Professional Liability and other specialty lines

Kinsale also writes policies in professional liability, general liability, and other specialty lines, which contribute to the remaining percentage of their gross written premiums.

These policies are designed to protect businesses and professionals in a variety of fields, such as technology, healthcare, and legal services, against malpractice, negligence, and other professional risks.

Geographical Revenue Distribution

Kinsale is a U.S. focused insurance company and operates exclusively within the United States.

The company has built a strong presence in the U.S. Excess & Surplus (E&S) market, where it benefits from the flexibility to write policies for a wide range of risks that are typically underserved by standard insurers.

The company does not currently operate internationally, focusing its efforts on mastering the U.S. market, which offers ample growth opportunities due to the large number of businesses in need of specialized coverage.

While Kinsale’s revenue is entirely derived from U.S. operations, the company’s geographic concentration gives it the advantage of being highly focused and adaptable to the specific needs of U.S. businesses. This allows them to efficiently allocate resources and tailor products to their customers.

Moat

Kinsale has built a strong competitive advantage within the E&S insurance market, thanks to its niche underwriting expertise, strong brand recognition, and disciplined risk management.

Several key factors contribute to Kinsale's moat:

Specialization

Kinsale has focused its resources on the E&S market, where it can take on more complex and higher-risk policies that traditional insurers are not equipped to handle. This specialization allows Kinsale to command higher premiums and avoid competition with more generalist insurance companies.

Underwriting expertise

The company has a long history of underwriting success, as evidenced by its consistently low combined ratio (indicating underwriting profitability). Kinsale’s ability to select and price risks appropriately is a significant competitive advantage in an industry where underwriting mistakes can be costly.

Brand and market position

Over time, Kinsale has built a strong reputation in the E&S space. This allows the company to attract top tier clients and expand its market share, benefiting from brand recognition in a highly specialized field.

Financial strength

Kinsale’s strong financial position, marked by its rising revenues and healthy reserves, makes it an attractive partner for brokers and policyholders. It also enables the company to withstand market fluctuations and pursue growth opportunities, further strengthening its moat.

Future Outlook

Looking ahead, Kinsale is well-positioned to capitalize on the continued growth of the E&S market, driven by increasing demand for specialized insurance products in sectors like technology, construction, and cybersecurity. The ongoing digital transformation and higher exposure to emerging risks are likely to create more opportunities for insurers like Kinsale to offer tailored solutions.

The company’s future growth will also benefit from the ongoing trends in risk mitigation, as businesses continue to seek coverage for emerging and evolving risks such as cybersecurity threats, climate-related risks, and global supply chain disruptions.

Kinsale’s underwriting discipline, strong market position, and ability to offer flexible solutions will allow it to grow its business in these high demand areas.

Kinsale’s focus on technology and data analytics for pricing and risk assessment will also help improve underwriting efficiency and profitability in the long term, positioning the company well in an increasingly data driven world.

Final Thoughts

Kinsale Capital has established itself as a leading player in the U.S. E&S insurance market, leveraging its underwriting expertise, financial strength, and specialization to consistently generate strong revenue and profits.

The company’s future outlook is promising, driven by continued demand for non-standard insurance products and the evolving risk landscape. With a clear competitive advantage and a disciplined approach to risk management, Kinsale is well positioned to continue benefiting from the growing demand for specialized insurance solutions.

Thank you for reading this article! If you enjoyed reading it, make sure to SUBSCRIBE so you don’t miss out any posts! And share, leave a comment!

If you enjoyed reading this article, you might enjoy these other ones to:

Disclaimer:

The content of this analysis is for informational purposes only and should not be considered financial or investment advice. The opinions expressed are my own and based on publicly available information at the time of writing. Before making any investment decisions, please conduct your own research or consult with a professional financial advisor to assess your individual situation. Investing in the stock market involves risk, and past performance is not indicative of future results.

Disclosure: I’m not invested in this business.

Great write-up! I am looking into this company myself, but I currently own a different insurer. Not sure if you invest outside of the U.S., but you might want to take a look at Protector Forsikring. It is a Norwegian based insurance company that also operates in the UK, France, Sweden, Denmark and Finland. They reported a combined ratio of 85.9% in Q1 25 and for FY24 they had a combined ratio of 91.2%. Their 3-year revenue growth CAGR is 26.7% and their 10-year is at 19.4%. Kinsale's ROIC 5-year avg is 8.4% and ROE 5-year avg is 28.2%, Protector has a ROIC 5-year avg of 17.9% and their ROE 5-year avg is 38.6%. Currently, I think Protector looks cheaper, but Kinsale grows quite a bit faster. I think both companies are great, and would love to hear your thoughts on how you compare them!

Great article, Felix. It’s definitely one of the best companies on the market.