Synopsys: A High-Quality Business on My Radar

This is my first stock analysis on Substack. Normally, I focus on breaking down market trends in tweets, but I wanted to start documenting my thought process on high-quality businesses in more detail.

Right now, I don’t own Synopsys ($SNPS), but it’s been on my radar for a while. My portfolio includes a range of businesses across different industries, and I’m always looking for companies with strong fundamentals, pricing power, and long-term growth potential. Synopsys checks those boxes, so I decided to take a closer look.

The company just reported its fiscal Q1 earnings on February 26, meeting expectations with solid execution. Its long-term trajectory remains strong. But despite delivering double-digit revenue and EPS growth, SNPS stock hasn’t performed well—down 15% in 2024 and 8% year-to-date. It’s trailing both the semiconductor sector and the broader market, even as its fundamentals stay intact.

Today, I will talk about the following:

Why SNPS is one of the best business in the semiconductor space

Business model

The importance of Electronic Design Automation (EDA)

Why customers can’t live without SNPS

Q1 25’ performance and key highlights

Ansys acquisition

Final Thoughts

That said, based on what I’ve seen so far, I’m bullish on the business. This isn’t an investment recommendation —just an analysis to determine whether it could be a good addition to my portfolio in the future. Now, let’s get into it.Why Synopsys Is One of the Best Compounding Businesses in The Semi Space

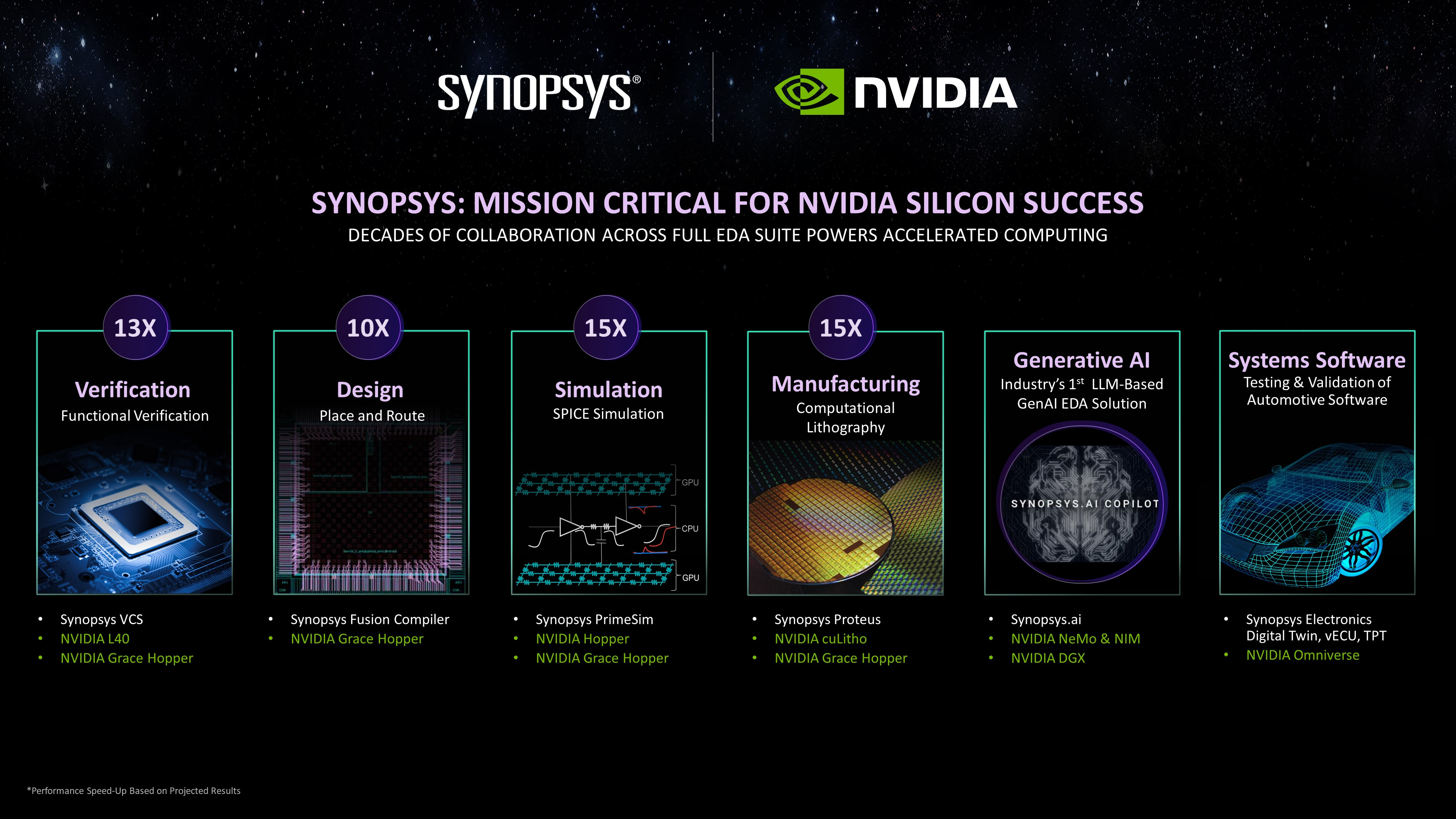

Synopsys is one of the highest-quality companies in the semiconductor space. It benefits from powerful secular trends, operates in an anti-cyclical niche within a highly cyclical industry, and runs on a subscription-based model. More importantly, its software is essential for chip designers like Nvidia, AMD, Broadcom, and Intel. No matter the market conditions, these companies rely on Synopsys tools to function.

This is a rock-solid business with long-term tailwinds, making it one of my highest-conviction picks for the decade ahead.

Yet, despite its strong fundamentals, SNPS stock is now trading at multi-year low multiples—far below historical valuations and my fair value estimate. And this is happening even as the company continues to execute at a high level.

So in this deep dive, I’ll break down Synopsys’ recent performance, financial health, growth outlook, and valuation. But first, a quick look at what makes this business so unique.

What Does Synopsys Do?

Synopsys is a leading company in the fields of Electronic Design Automation (EDA) and Semiconductor Intellectual Property (IP), both essential for designing and manufacturing modern electronic devices like smartphones, computers, and other digital technologies.

1. Electronic Design Automation (EDA)

EDA refers to the software tools used by engineers to design and analyze electronic systems, particularly integrated circuits (ICs), commonly known as chips. These tools help in creating the complex blueprints of chips that power various electronic devices.

Synopsys provides a suite of EDA tools that assist engineers in designing chips efficiently and accurately. In the fiscal fourth quarter of 2024, Synopsys reported a 17% year-over-year revenue increase in its chip design segment, highlighting the growing demand for advanced EDA solutions.

Software | Altair")

2. Semiconductor Intellectual Property (IP)

Semiconductor IP consists of reusable components or cores used in chip designs, such as processors, memory interfaces, and connectivity solutions. These pre-designed elements allow companies to integrate complex functionalities into their chips without starting from scratch, saving time and resources.

Synopsys offers a range of IP solutions that are integral to modern chip designs. Despite facing stiff competition from companies like ARM, Synopsys has been making significant strides in the IP market, closing the gap by 13.6 percentage points over six years, with its IP revenue growth surpassing ARM's by 10.8 percentage points during the same period.

Top 5 companies in the semiconductor IP market by market share:

Recent Financial Performance

In December 2024, Synopsys reported its financial results for the fourth quarter and fiscal year 2024:

Q4 2024: The company achieved record quarterly revenue of $1.636 billion, an 11% increase compared to the same quarter the previous year. Adjusted earnings per share (EPS) were $3.40, a 13% year-over-year rise.

Fiscal Year 2024: Full-year revenue reached $6.127 billion, up 15% from the prior year. Synopsys also improved its operating margins and delivered a 25% increase in adjusted EPS.

Looking Ahead

Synopsys projects continued growth, expecting double-digit revenue increases in 2025. The company is also preparing for the anticipated acquisition of Ansys, a leader in simulation software, aiming to enhance its capabilities in chip design and other engineering fields. This acquisition is expected to close in the first half of 2025, pending regulatory approvals.

Conclusion

Synopsys is crucial to the semiconductor industry, offering key tools and components that drive the design of cutting-edge electronic devices. The company's strong focus on innovation and strategic growth puts it in an excellent position to address the ever-evolving technological landscape. Most notably, the core strength of Synopsys lies in its EDA software, which makes up around 70% of its total revenue.

Why EDA Is So Important For Semiconductor Design

Electronic Design Automation (EDA) software is a crucial tool in the semiconductor industry, allowing engineers to design, test, and refine complex chips before they are manufactured. But its impact extends far beyond chip design—it plays a key role in advancing several high-growth industries:

Automotive: AI, IoT, and cloud computing are revolutionizing vehicle technology, enabling smarter, safer, and more autonomous cars. EDA tools help develop the advanced semiconductor components that power these innovations.

Artificial Intelligence (AI) & Internet of Things (IoT): AI and IoT rely on increasingly sophisticated chips to process and analyze vast amounts of data. EDA software ensures these chips are designed for maximum efficiency and performance, supporting everything from smart home devices to industrial automation.

Cloud Computing: The growing demand for cloud services requires powerful data center chips. Cloud-based EDA solutions make it easier and more cost-effective for semiconductor companies to design cutting-edge processors that drive cloud infrastructure.

5G: The next generation of wireless communication depends on highly specialized semiconductor technology. EDA tools enable the development of 5G-compatible chips, ensuring faster and more reliable connectivity for devices worldwide.

The Complexity of Contemporary Chip Design

Modern semiconductor chips are marvels of miniaturization and complexity. For instance, Apple's M4 chip, released in 2024, boasts a transistor count of approximately 28 billion.

This scale of integration necessitates sophisticated design tools to manage the vast number of components and their interconnections.

Synopsys' Advanced EDA Solutions

Synopsys' EDA software extends beyond basic design functionalities. It offers capabilities to simulate and verify chip performance at the physics level, which is increasingly vital as semiconductor technology approaches physical and quantum limits. This ensures that designs not only meet performance benchmarks but also adhere to the fundamental laws of physics.

Market Dynamics and Competitive Landscape

The EDA market is predominantly controlled by a few key players, with Synopsys and Cadence Design Systems leading the charge. Together, they hold a substantial share of the global market, with Synopsys experiencing growth in its market share in recent years.

This duopoly is reinforced by significant barriers to entry, including the need for extensive research and development and a deep reservoir of specialized knowledge.

Challenges for Emerging Competitors

Developing a competitive EDA suite akin to those of Synopsys or Cadence is a formidable endeavor. It requires decades of dedicated R&D and an immense accumulation of expertise. Consequently, new entrants face significant challenges in penetrating this market, allowing established companies like Synopsys to maintain a robust and enduring competitive advantage.

In summary, EDA software is the backbone of semiconductor design, and Synopsys plays a pivotal role in this domain. Its advanced tools and strategic position enable the creation of increasingly complex and efficient chips, powering the next generation of electronic devices.

Why Customers Can’t Live Without Synopsys

Synopsys' software is indispensable in the semiconductor industry, playing a crucial role in the design and verification of complex integrated circuits. The company's Electronic Design Automation (EDA) and semiconductor Intellectual Property (IP) products are deeply integrated into the workflows of leading technology firms

Mission-Critical Tools for Industry Leaders

Industry leaders like NVIDIA consider Synopsys' tools essential for their operations. Jensen Huang, CEO of NVIDIA, has referred to Synopsys' EDA and IP products as "mission-critical," highlighting their importance in developing cutting-edge technologies.

Resilient Business Model with Steady Growth

Synopsys' subscription-based revenue model offers stability, as customers rely on these tools for ongoing projects, making it difficult to discontinue services without significant setbacks. This resilience has contributed to Synopsys' consistent revenue growth over the years, even amidst the semiconductor industry's cyclical fluctuations. For instance, despite a challenging fiscal fourth quarter in 2024, Synopsys reported adjusted earnings per share of $3.40, surpassing expectations.

Significant Backlog and Financial Strategy

As of early 2025, Synopsys has a non-cancellable backlog nearing $10 billion, providing clear visibility into future revenues. To further strengthen its market position, Synopsys is preparing to issue approximately $10 billion in bonds to finance the acquisition of Ansys, a move expected to enhance its simulation capabilities and open new revenue streams.

Growing Demand Amid Technological Advancements

The increasing complexity of semiconductor design, driven by advancements in Artificial Intelligence (AI), High-Performance Computing (HPC), and sophisticated chip architectures, is expanding the demand for Synopsys' tools. As these technologies evolve, the necessity for robust design and verification solutions becomes more pronounced, ensuring Synopsys' integral role in the industry's future.

Q1 Performance & Key Highlights

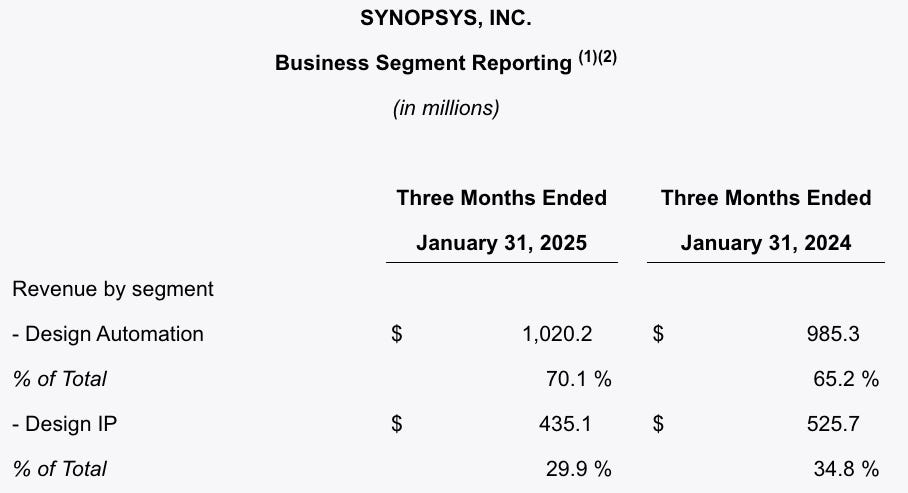

Revenue: Synopsys reported first-quarter revenue of $1.46 billion, a 4% year-over-year (YoY) decline, aligning with analyst expectations.

EDA Revenue: The Electronic Design Automation (EDA) segment generated $1.02 billion, reflecting a 4% YoY increase, driven by sustained investments in research and development (R&D) from customers.

IP Revenue: Intellectual Property (IP) revenue was $435 million, a 17% YoY decrease, influenced by challenging year-over-year comparisons and the shorter quarter.

Source: Synopsys, 2025

Adjusted Revenue for Shorter Quarter

The revenue decline appears more pronounced due to Q1 2025 having one fewer week than Q1 2024. Adjusting for this discrepancy, Synopsys achieved high-single-digit revenue growth, indicating robust operational performance.

Product Innovation & AI Integration

Synopsys continues to innovate with products like PrimeTime and IC Validator, delivering significant efficiency improvements for customers. The integration of Artificial Intelligence (AI) has become increasingly important, both in driving demand for Synopsys' tools and enhancing its software capabilities. Early AI integrations have already resulted in 2-4x efficiency gains, underscoring the potential for further advancements.

Financial Metrics

Operating Margin: The operating margin stood at 36.5%, a 220 basis points (bps) decrease YoY, primarily due to the shorter quarter.

Earnings Per Share (EPS): EPS was $3.03, a 10% YoY decline, but $0.24 above estimates, representing a 9% earnings beat.

Free Cash Flow (FCF): FCF was -$108 million, a temporary decline expected to normalize in subsequent quarters.

Cash & Investments: Synopsys maintains a strong liquidity position with $3.81 billion in cash and investments.

Debt: The company holds minimal debt, totaling $665 million.

Outlook

Synopsys projects Q2 revenue between $1.59 billion and $1.62 billion, slightly above analyst expectations. Adjusted EPS is anticipated to be between $3.37 and $3.42, higher than the estimated $3.35. The company continues to benefit from rising demand for AI chip design, collaborating with major players like NVIDIA, Qualcomm, and Intel.

Strategic Developments

Synopsys is advancing its $35 billion acquisition of Ansys, having received approval from the European Union and engaging with Chinese regulators. This acquisition aims to enhance Synopsys' simulation capabilities and open new revenue streams, reinforcing its position in the semiconductor design industry.

Conclusion

Despite the temporary challenges posed by a shorter quarter, Synopsys demonstrates resilience and growth, driven by innovation and strategic investments in AI and acquisitions. The company's strong financial position and positive outlook underscore its pivotal role in advancing semiconductor design technology.

Acquisition of Ansys

Synopsys is set to acquire Ansys, a leader in engineering simulation software, in a cash-and-stock transaction valued at approximately $35 billion. This strategic move aims to expand Synopsys' capabilities from semiconductor design to comprehensive system-level simulation, creating an integrated silicon-to-systems platform.

Financing the Acquisition

To finance the acquisition, Synopsys is preparing to issue approximately $10 billion in bonds. The company has engaged major financial institutions, including Bank of America, HSBC Holdings, and JPMorgan Chase, to organize discussions with fixed-income investors.

Strategic Implications

The integration of Ansys' simulation and analysis expertise with Synopsys' semiconductor design technology is expected to:

Enhance Product Offerings: Provide a holistic approach to innovation, addressing the increasing complexity in electronics and physics, augmented by artificial intelligence (AI).

Expand Total Addressable Market (TAM): Increase Synopsys' TAM by 1.5 times to approximately $28 billion, with an expected compound annual growth rate (CAGR) of about 11%.

Improve Financial Performance: Deliver high-growth, high-margin, recurring revenue, with anticipated expansion of non-GAAP operating margins by approximately 125 basis points and unlevered free cash flow margins by about 75 basis points in the first full year post-closing.

The acquisition is anticipated to be accretive to non-GAAP earnings per share within the second full year post-close and substantially accretive thereafter.

Conclusion

With financing plans underway, Synopsys is on track to finalize the acquisition of Ansys in the first half of 2025. This strategic move is poised to solidify Synopsys' leadership in AI-driven semiconductor and system design, offering a comprehensive suite of solutions from silicon to full system-level simulation.

Final Thoughts

Synopsys stands out as a dominant force in the semiconductor ecosystem, offering essential tools that enable the design of the world’s most advanced chips. The company benefits from a resilient business model, high switching costs, and strong secular tailwinds in AI, high-performance computing, and advanced semiconductor manufacturing. Despite near-term stock underperformance, its fundamentals remain strong, and the upcoming Ansys acquisition could unlock significant long-term value.

As someone who prioritizes high-quality businesses with pricing power and durable moats, Synopsys checks many of the right boxes. While I don’t own the stock yet, my deep dive has reinforced my conviction in its long-term potential. It remains firmly on my watchlist, and I’ll be keeping a close eye on its execution, valuation, and the impact of its strategic moves going forward.

To further evaluate its long-term investment potential, I’ll be doing a deep dive into Synopsys’ fundamentals, breaking down its financials, competitive positioning, and growth outlook in more detail. Make sure to follow so you don’t miss it and to see more content coming your way.

Insightful deep dive with solid points on why $SNPS is a fantastic company. It unfortunately hasn’t shown that in the stock price. I continue to hold.